The topic du jour of the Berlin startup scene has changed from 2013’s “Is Berlin all hype?” to 2014’s “When is Berlin’s big exit?”

From Peter Thiel’s talk at Hy Berlin, to Bloomberg predicting four possible Berlin IPO’s in 2014 (two of which happened), exit expectations are everywhere. It is no longer if, but when. Along with the anticipation, a consensus is growing that exit events are a necessary step for Berlin to prove itself as a legitimate ecosystem.

Why do big exits matter? There are several reasons. First, international investors will pay more attention. The lure of high returns will get American VC’s on planes, and just maybe AirBerlin will bring back the non-stop Tegel to SFO flight (fingers crossed for all of us).

The other critical reason? Equity. While this does not receive nearly as much attention as the presumed inflow of new American investment, the truth is that – assuming that employees have equity – exits flood money into the ecosystem.

In that scenario, IPO’s can mean dozens, if not hundreds of new millionaires eager to invest in both new startups and real estate. According to Bloomberg, Facebook’s IPO created 850 new millionaires, many of whom “decided to invest their wealth in emerging technology companies such as Instagram Inc., Spotify Ltd. and Flipboard Inc.” Twitter’s initial public offering created some 1,600 millionaires, or two-thirds of the company.

Did the same happen when Zalando and Rocket Internet went public? Not that we’ve seen yet. I sat down with Kevin Dykes, an American who built his latest company, RetentionGrid, in Berlin. Kevin explained that, in the US, it is an expected practice for a company to have a stock option program from day one, available to everyone. In key markets like San Francisco, New York or Austin, options are a must-have for recruiting purposes. Upon exit, those options create a new generation of angels that start their own companies or use that money to invest. And why not? As Kevin says, “This shit is hard and skin in the game is important.”

American exits mean loyal employees and more money feeding the ecosystem. Sounds great, right? So why hasn’t it taken off in Berlin? Kevin speculates that, culturally, equity just isn’t as desired in Germany. “It hasn’t been a requirement of any hiring conversation so far.” He views this as a limiting factor in Berlin, where most of the angels you meet were founders, not former employees.

This was seconded recently by Dominik S. Richter Founder & Global CEO of HelloFresh. After raising a $50 million round, he told Venture Village, “Here, high performing employees often do not appreciate and value stock and stock options correctly, thus making it hard for early stage startups to win over great talent from more established industries or players who can pay better salaries. I think this due to the fact that not a lot of wealth has been created through stock in Berlin so far, i.e. lack of role models, but I hope this will change if we have a couple of good exits in Berlin.” The situation now looks like the chicken and the egg – Berlin needs exits to demonstrate how much Berlin stands to gain from exits.

Equity in Berlin also has challenging tax regulations that have not yet been tested (surprise, surprise). Instead of a traditional option pool like you would find in the US, Germany uses a virtual equity model which has implications for payout and reinvestment.

In Berlin, Equity Is Virtual

I met with serious experts Rainer Weichhaus and Konstantin Maretis of RoeverBroennerSusat, one of Germany’s leading independent audit and tax consultancy firms. And let me say that, as someone who has dealt with my fair share of questionable lawyers and tax accountants in Germany, these guys know their shit.

Konstantin explained that the typical American option pool program is not usually offered in Germany due to differing legal regulations. In Germany, most startups work with virtual stock programs, rather than direct equity. Employees are granted virtual shares of the company, at a fixed price at a certain point in time. Upon exit, the shareholder sells their shares and the employee is treated as if he would have sold real shares.

Rainer explained that this is quite an easy way to handle participation because, while employees are, in a way, shareholders, they do not receive shareholders rights. For instance, they will never sit in shareholders meetings. They become actual shareholders only when an exit occurs.

Both Rainer and Konstantin say that they see most German startups implementing similar programs, especially for early employees, such as the first twenty-five to join the company. “At the end of the day you only have one cake and you can only share it once.”

There are also tax considerations: American stock options are subject to wage tax immediately. In Germany, the tax is only levied if there is a payment. There are different tax rates for wages and for shareholder positions. The list goes on.

The American Equity Model

In the beginning, equity is more art than a science.

Fred Wilson writes: “Once you have assembled a core team that is operating the business, you need to move from art to science in terms of granting employee equity. And most importantly you need to move away from points of equity to the dollar value of equity… The key thing is to communicate the equity grant in dollar values, not in percentage of the company… Talking about grants in dollar values emphasizes that equity aligns interests around increasing the value of the company and makes it tangible to the employees.”

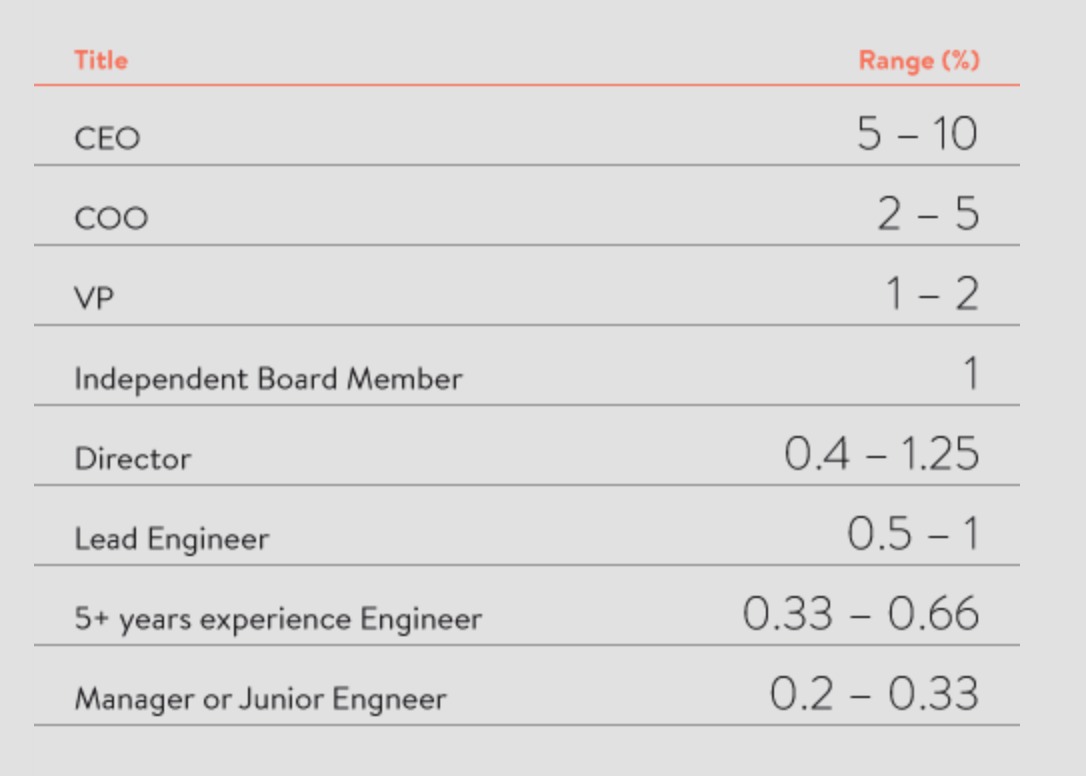

Typically, between 10-15% is distributed to employees in the seed round. Once you hit Series A, 20%-25% of the company is allotted for employees. This may seem like a lot, but it encourages even more in good will. What does the breakdown look like? Tony Karrer included this option shuffle breakdown on his blog:

How Common is Equity in Berlin?

How Common is Equity in Berlin?

While my friends at RoeverBroennerSusat saw the startups they worked with offering equity in Berlin more often than not, I thought that I would verify independently. I spoke with dozens of founders, employees, recruiters and lawyers, many of whom provided information as long as it was off the record.

I met with Jeremy Del-Guidici, CEO at VonChurch Berlin GmbH, a leading recruiting firm that specializes in helping digitally focused companies evolve. The company was originally started in San Francisco in 2008 and arrived in Berlin last year. Jeremy deals with startups of all sizes and agrees that startup equity models in Berlin are dramatically different than those in the States or the UK.

Out of all VonChurch’s Berlin startup clients, Jeremy estimates that less than 5% offer equity across the board to early employees, and less than 10% offer equity when hiring senior positions. With virtual stock, the number is closer to 0.1%.

None of the founders I interviewed, who had raised a seed round, had implemented a virtual equity model, though many were interested or actively working with tax advisors to set one up. Across the board, founders expressed confusion on what percentages to offer.

I spoke to three startups which had raised over one million euros. One was in the process of implementing traditional stock options. Though they are based in Berlin, they are a limited UK company, and their American and UK investors had required it. The second company was a Gmbh that used the virtual equity model, but as an incentive for senior hires rather that first employees. “Our first employees were an intern, a junior developer and then a intermediate frontend developer. So, it wouldn’t make sense to give them stock options. Besides we had enough financial resources to motivate them by their salary and didn’t need the “extra” motivation through stock options.” The third company is a thriving B2C company. They give options to most of their employees, not just first employees. The initial pool was 5%, but they’ve topped that up with every funding round since.

While German startups are starting to think about equity, there is no standard model yet, and company policies vary widely.

The Times They Are A’ Changing

Everyone agreed that, as time goes on, equity will become the norm here in Berlin. Jeremy of VonChurch predicts that the market will naturally push in that direction. If recruiters are calling with offers for the same salary plus equity, you will be more willing to talk to your current employer about options.

The influx of international workers and American and UK investment will speed things up. More startups will have to compete with companies abroad for quality talent, and that means offering stock. US investors expect, and oftentimes require, early employee stock options. Several of the companies I spoke to were implementing programs at the encouragement of their investors.

It’s also the right thing to do. 6Wunderkinder CEO Christian Reber writes about this in his popular blog. He recommends giving away 10-20 percent for employees. “Be generous with shares to your employees, they are your capital and most important resource. But never give away shares without clear vesting rules. When it comes to equity, be fair. Everyone should invest the same energy and the same amount of time.”

Berlin’s big exits are coming. They could make a few people very rich, or jump start the next generation of hot companies. More millionaires with startup experience are one key to continuing the growth in Berlin.

This article was originally published on Hack&Craft News.

Recent Comments